For some people who set out to define “enough” and set a limit for their spending, there is one looming barrier to getting started. Debt. Over 80% of Americans have some form of debt (including mortgages). For those with personal (non-mortgage) debt, the average owed is a staggering $38,000.

Perhaps you have some significant debt yourself, whether that’s credit card debt, student loans, car payments, or something else. If that’s the case, how are we supposed to commit to setting a limit for our spending?

Below, we’re going to cover the major types of debt and how you should think of each.

Current (Existing) Debt

The debts and loans that we have right now will tend to fall into two major categories.

Unsecured Debts

(no Collateral)

- Student loans

- Credit card debt

Secured Debts

(with Collateral)

- Mortgage (house)

- Auto loan (car)

What is significant about these two groups? The debts in the left column represent money you’ve borrowed that is not tied to an item (collateral). If you are unable to pay an unsecured debt, there is nothing for the lender to seize (though they can still ruin your credit rating!). A good example of unsecured debt is student loans.

The debts on the right, however, represent money that you’ve borrowed that is tied to an item. The item, like a house or car, is called collateral. If you don’t pay these debts, your lender can seize the collateral as payment.

When considering how we manage the money God has entrusted to us, these two types of debt are treated differently. While we will cover both in detail, the main difference lies in the fact that at any point, we could decide that a secured debt was no longer worth it, and could sell the item to quickly pay off the loan. For example, if we purchased a house that was much too expensive, it is possible to sell the house later on and purchase a more reasonably-priced house instead. On the other hand, if we have an overwhelming amount of student loans, there is really no option other than paying them off.

UNSecured Debts

We acquire debts for all sorts of reasons, some good, some bad. Regardless of the reason, however, unsecured debt like student loans or credit card debt can become a significant barrier to our ability to give freely and participate in the work God is doing.

Because of this barrier, we have a simple approach to handling these types of debt: pay them off now. Don’t worry, we have a couple straightforward steps to get you there.

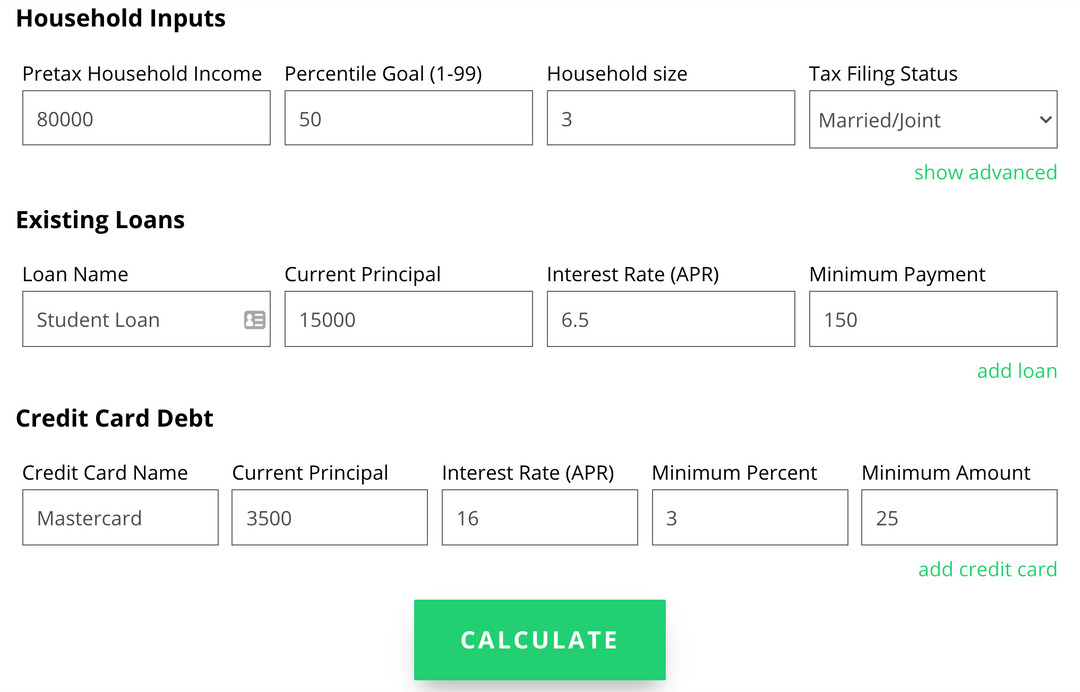

To walk through the process, let’s consider a theoretical family of 3 with an income of $85,000 per year. They have student loans and some credit card debt. They’ve also chosen to limit their spending to the 50th percentile.

Using the Calculator: Head over to the Debt Payoff Calculator. Enter in the inputs below. Remember, only unsecured debts should be included in the payment plan. Therefore, the family would include their student loan and credit card debt for the calculator, but not their mortgage or car loan. We’ll discuss those later.

Reviewing the Plan: Look at the results and see how long it would take the family to be debt free if they set their standard of living to the 50th percentile. Notice also that the debts are ordered by interest rate, highest to lowest, in the results to help you know which to pay off first. While there are a number of ways to pay down debt, this strategy ends up costing the least overall. Try entering a few different percentiles to see how the results change.

Implementing the Plan: To put things into action, the family would do the following:

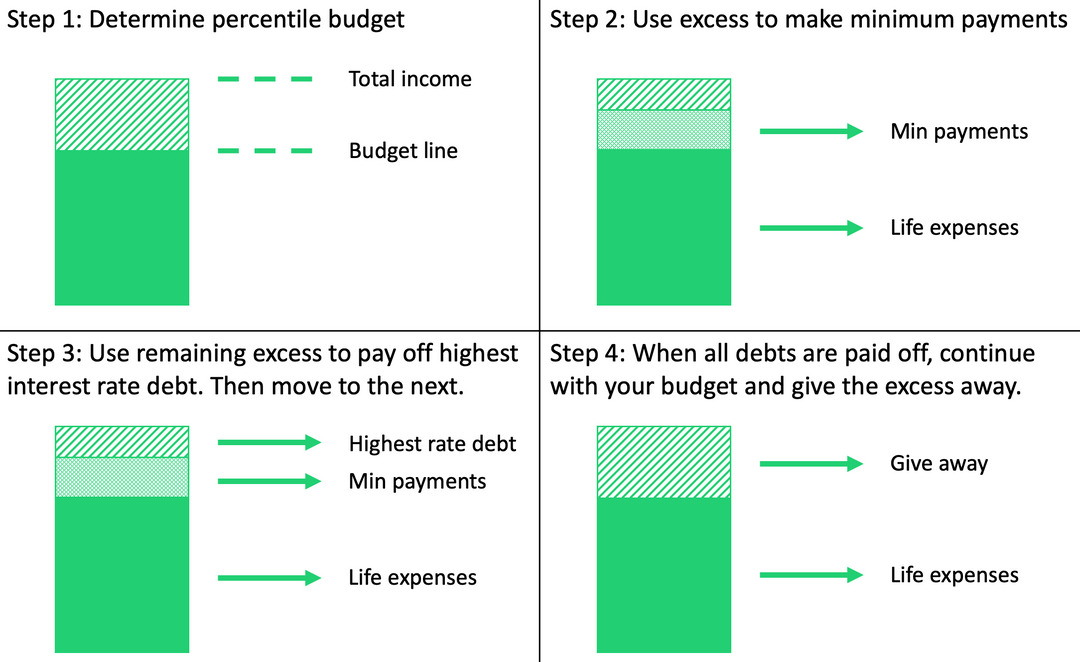

Step 1: Reduce their expenses to the monthly budget for the 50th percentile, $4,828. These are their operational costs.

Step 2: Use the excess $894 above their operational cost budget to pay the minimum balances due on each of their debts ($255 in all) to avoid any late fees or penalties. If there was not enough excess to cover minimum payments, they would have had to use some of their operational cost budget to cover those. Make sure the minimum balance gets paid!

Step 3: Use the remaining $657 of the excess to make additional payments on their unsecured debts, starting with the debt with the highest interest rate. When that is paid off, start on the next highest until all are paid off.

Step 4: When all debts are paid off, continue living at the 50th percentile and begin giving away the excess $894.

Now that you’ve worked through an example, try using your own debt information. Once you’ve entered all your information, try out a few different percentiles to see how the payoff time and plan change. Remember, don’t include secured debts like your mortgage or car payments.

Secured Debts

While secured debts like a mortgage or car loan may also prevent us from giving or participating in the work God is doing, there is a significant difference from the prior category. These debts require an ongoing decision that the item we purchased is still worth having the loan.

For that reason, we recommend that these debts should generally be included in the monthly percentile budget that we worked with last week. Let’s use a car loan as an example.

Many factors go into buying a car, and there are many options available across a wide price range. When we purchase a car, we are saying that all of the features of that vehicle are worth the money we paid for it.

After the initial purchase, we always have the ability to sell the car, use the money to pay off the remainder of the loan, and buy a different car. Every day that we keep that car, we are saying that it continues to be worth the money we paid for it (and it very well may!). Of course, there are some other factors, like depreciation, changing needs, etc., that come into play. But the general principle holds true.

Since the car purchase requires this sort of ongoing decision, we make our auto loan payments out of our monthly budget, our operational costs. Each month, the car continues to be one of our operational costs. And each month, we make the decision that we must set aside some of the money God has placed in our hands to cover the cost of that car. The same could be said of our house, or other large purchases requiring a loan like this.

As we start looking at defining “enough” and setting a limit to our spending, we might realize that some of these secured debts may pose barriers to managing God’s wealth in the way we would like to. Unsecured debts, like student loans, simply have to be paid off. There are no other options. But secured debts, like a house or car, can always be reconsidered.

Remember, God has given us a portion of his wealth to manage. But He doesn’t force us to manage it His way. Instead, He gives us room to figure things out. As we consider this responsibility, it is possible that some of us may come to the conclusion that our car, our house, or a similar large purchase is preventing us from investing in God’s kingdom to the degree we feel called to. So what do we do in that situation?

Picture. Try to picture how you would make the purchase from scratch. If you didn’t already have the car, house, etc that you already own, how would you go about finding one that allows you to give in the way you feel called?

Pray. Ask God to help you manage His wealth wisely. And ask Him how you should approach any of these debts you feel called to reconsider. Lift these items up to Him often and offer them to Him to do with what He sees fit.

Plan. Start to work out how to get to where you want to be. Are you already planning a move in a year or two? Maybe you can bring your mortgage payments closer to your goal at that time. Is the end of the year coming up, when car prices are at their lowest? That might be a good time to look for a more suitable car.

These are big decisions, just like they were big decisions the first time we purchased a car or home. And making changes takes time, patience, and wisdom. Each of us alone is responsible for the money God has placed in our hands. And ultimately, the way we manage it is between us and God.

0 Comments